The key tax measure announcements include:

- Personal tax thresholds are frozen until 2022. Increases are promised in 2022, with a further freeze until 2026.

- From 2023 the Corporation Tax rate will increase to 25%. The current rate of 19% will continue to apply to small businesses with profits of £50k or less. A tapered rate will apply to companies with profits of between £50k and £250k.

- Companies will be able to carry back losses for three years, to secure repayment of tax paid in prior years.

- A super-deduction (Capital Allowance) for business investment at 130% of costs, for companies, will apply for two years.

- The nil rate band for Inheritance Tax, the Lifetime Limit and Annual Allowances for pensions, and the VAT registration threshold are all frozen.

- The Coronavirus Job Retention Scheme (furlough scheme) is extended to the end of September, with a 10% contribution from employers for July and August, and 20% for September. Employees will continue to receive 80% of salary for unworked hours.

- Self-Employed Support Scheme extended, with grants 4 and 5. The newly self-employed who have submitted 2019-20 tax returns can apply. An 80% grant continues to apply where profits are reduced by 30% or more. A 30% grant will apply where profits are reduced by less than 30%.

- Stamp Duty Land Tax (SDLT): the £500k nil rate band is extended to 30 June. A £250k nil rate band will then apply until 30 September.

- The 5% rate of VAT for the tourism and hospitality sectors is extended to 30 June. An interim rate of 12.5% will then apply until April 2022.

- New restart grants of £6k for non-essential retail businesses and £18k for hospitality businesses will be available from April.

- Business rates holiday for the retail, hospitality and tourism sectors is extended to 30 June. A two-thirds discount will then apply for the rest of 2021/22.

- Investment in HMRC to tackle COVID-19 support fraud and tax avoidance.

INTRODUCTION

On some counts this Budget was Rishi Sunak’s 15th major Rishi Sunak has delivered a targeted balance of new tax increases and tax reliefs as he tries to support struggling sectors and stabilise the national debt.

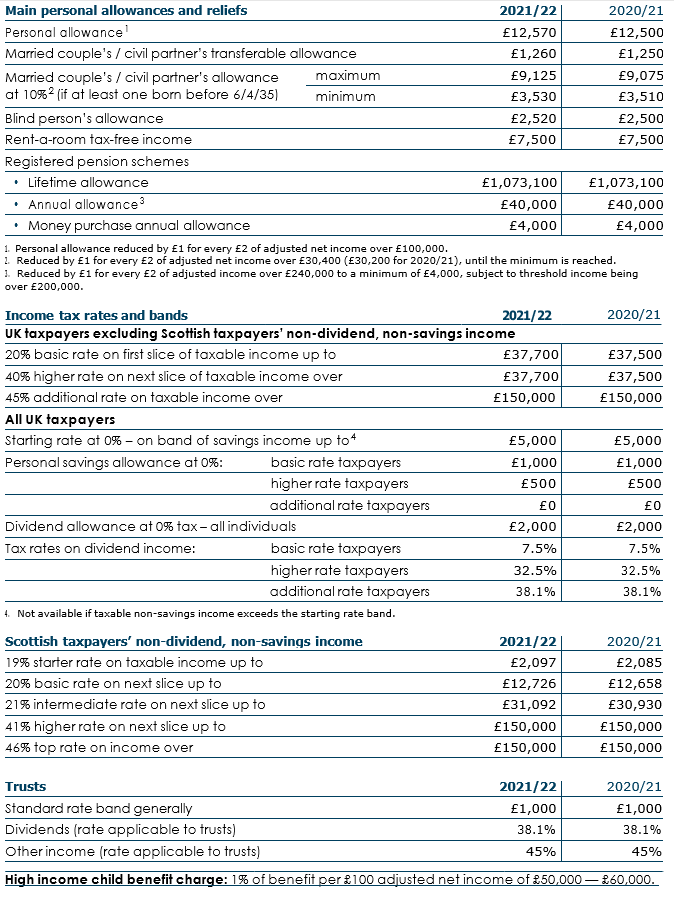

Although the income tax, CGT and national insurance rates remain unchanged, the personal allowance and the higher rate threshold will be frozen from 2021/22 to 2025/26.

Businesses will enjoy the new ‘super deduction’ on capital investments and the temporary three-year carry back on losses. The corporation tax rate, however, will be increased to 25% from April 2023 – though smaller businesses will be protected from this tax burden by a new small profits rate.

It will be interesting to see the further tax announcements that will be made on 23 March, when the Chancellor lays out new tax consultations and calls for evidence. These may provide more insight into the future direction of the Government’s tax policy for the UK.

PERSONAL TAXATION

PERSONAL TAXATION AND INVESTMENTS

Income tax

The personal allowance will rise to £12,570 and the higher rate threshold for 2021/22 will increase to £50,270, as previously announced. From 2022/23 to 2025/26, both the personal allowance and higher rate threshold will be frozen. In Scotland, the higher rate threshold for non-savings, non-dividend income will rise to £43,662 in 2021/22 as announced in the Scottish Budget.

National insurance contributions (NICs)

The NIC upper earnings limit and upper profits limit will remain aligned to the higher rate threshold at £50,270 for 2021/22 and through to 2025/26.

Taxation of payments under the self-employment income support scheme (SEISS)

Grants from the SEISS made on or after 6 April 2021 will be taxed in the year of receipt regardless of the accounting year end. Legislation in the Finance Bill will ensure this measure has effect for the tax year 2020/21 and for subsequent tax years.

Income tax exemption for employer-reimbursed COVID-19 tests

There will be an income tax exemption for payments that an employer makes to an employee to reimburse the cost of a relevant coronavirus antigen test in 2020/21 (retrospectively) and 2021/22. The corresponding NIC disregard is already in force for 2020/21 and will be extended to 2021/22.

Easement for employer-provided bicycles exemption There will be a time-limited easement to the employer-provided cycle exemption to remove the requirement that employer- provided cycles be used mainly for journeys to, from or during work. The easement will be available to employees who have joined a scheme and have been provided with a cycle or cycling equipment on or before 20 December 2020. The easement will remain in force until 5 April 2022.

Mortgage guarantee scheme

A new residential mortgage guarantee scheme will run from April 2021 to December 2022, aimed at increasing availability of 91% to 95% loan-to-value mortgages.

The maximum property value will be £600,000 and mortgages must be arranged on a repayment basis.

Extension of social investment tax relief (SITR)

The government will extend the operation of SITR to April 2023.

Individual savings account (ISA) subscription limits

The ISA annual subscription limit for 2021/22 will remain at £20,000 and the corresponding limit for junior ISAs (JISAs) and child trust funds (CTFs) will stay at £9,000.

Green National Savings & Investments (NS&I) product

NS&I will offer a green retail savings product in summer 2021. It will be closely linked to the UK’s sovereign green bond framework, details of which are to be published in June 2021. The first green gilt will also be issued this summer.

Lifetime allowance

The lifetime allowance for pension savings will be frozen at £1,073,100 until April 2026.

Taxation of collective money purchase pensions

Legislation will ensure that collective money purchase pension schemes can operate as registered pension schemes for tax purposes. These are also known as collective defined contribution schemes (CDCs), to be introduced by the Pension Schemes Act 2021.

CAPITAL TAXES

Capital gains tax (CGT) annual exempt amount

The annual exempt amount for individuals and personal representatives will remain at £12,300 until 5 April 2026, and the amount for most trustees will likewise remain at £6,150 (minimum £1,230).

Inheritance tax (IHT)

The IHT nil rate band will remain at £325,000 until 5 April 2026. The residence nil rate band (RNRB) will likewise stay at £175,000 and the RNRB taper will continue to apply where the value of the deceased’s estate is greater than £2 million.

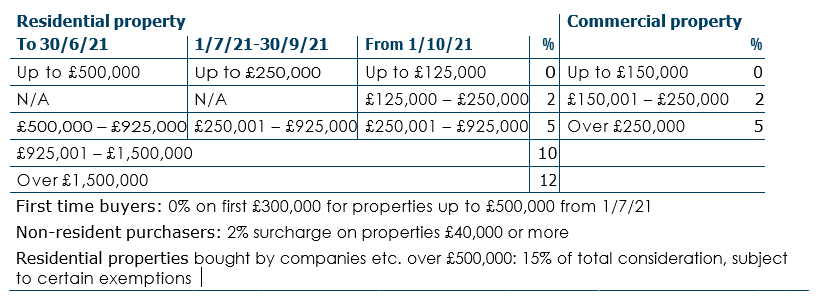

Stamp duty land tax (SDLT) temporary rates

The temporary increase to £500,000 to the SDLT nil rate band for residential property in England and Northern Ireland is extended until 30 June 2021. From 1 July 2021 until 30 September 2021, the nil rate band will be £250,000 and will then return to £125,000.

Non-UK resident SDLT

As previously announced, there will be an SDLT surcharge on non-UK residents buying residential property in England and Northern Ireland from 1 April 2021. The surcharge will be 2% above the existing residential rates.

SDLT on slices of value (England & N Ireland)

BUSINESS TAXES

Corporation tax, diverted profits tax and bank surcharge The main rate of corporation tax will remain at 19% for the year beginning 1 April 2022 and will rise to 25% from April 2023 for businesses with profits of £250,000 and over. The rate for businesses with profits of £50,000 or less will remain at 19% and there will be a marginal taper for profits between £50,000 and £250,000.

These thresholds are proportionately reduced for the number of associated companies and for short accounting periods. The rate of diverted profits tax will increase to 31%. The government will review the bank surcharge rate of 8% in light of the corporation tax increase.

Loss relief

The period over which incorporated and unincorporated businesses may carry back trading losses will be extended temporarily from one year to three years.

This extension will apply to a maximum £2 million of unused trading losses made in each of the tax years 2020/21 and 2021/22 by unincorporated businesses. The same maximum will apply separately to companies’ unused trading losses, after carry back to the preceding year, in relevant accounting periods ending between 1 April 2020 and 31 March 2021 and for periods ending between 1 April 2021 and 31 March 2022.

The £2 million cap will be subject to a group- level limit, requiring groups with companies that have the capacity to carry back losses above £200,000 to apportion the cap between their companies.

Research and development (R&D) tax credits

As previously announced, for accounting periods beginning on or after 1 April 2021, the amount of payable R&D tax credit that a small and medium-sized enterprise (SME) can receive in any one year will be capped at £20,000 plus three times the company’s total PAYE and NIC liability.

Super-deduction for investment in plant and machinery and 50% first-year allowances

Companies investing in qualifying new plant and machinery between 1 April 2021 and 31 March 2023 will benefit from new first-year capital allowances.

Investments in main-rate assets – those that qualify for 18% writing down allowance (WDA) – will be relieved by a 130% super-deduction, while investments in assets qualifying for 6% WDAs will benefit from a 50% first-year allowance.

Annual investment allowance (AIA) extension

As previously announced, the temporary £1 million limit for the AIA will be extended again – to 31 December 2021.

Freeports

Eight new English freeports have been announced: East Midlands Airport, Felixstowe and Harwich, Humber Region, Liverpool City Region, Plymouth, Solent, Thames and Teesside. Several tax reliefs will be available in designated tax sites within the freeports once these sites have been confirmed.

- Companies investing in plant and machinery will qualify for a 100% enhanced capital allowance. This will have effect for investment incurred on or after their designation as tax sites until 30 September 2026.

- An enhanced 10% rate of structures and buildings allowance will be available for constructing or renovating non-residential structures and buildings. The structure or building will have to be brought into use by 30 September 2026.

- Full relief from SDLT will apply until 30 September 2026 to the purchase of land for qualifying use in freeport tax sites in England once they have been designated.

- Full business rates relief will be available to all new businesses and certain existing businesses that expand, until September 2026. Relief will apply for five years from when the business first receives relief.

- Subject to parliamentary process, an employer NIC relief will be available for eligible employees from April 2022 until at least April 2026 and possibly up to April 2031.

Plant and machinery leases

Certain parts of anti-avoidance legislation affecting leases extended as a result of COVID-19 will be turned off. This will restore eligibility to claim capital allowances to the position as originally intended immediately before the date of the change in consideration due under the lease.

The change will affect leases only where a relevant change in consideration is implemented between 1 January 2020 and 30 June 2021. Either party may choose not to apply this treatment, the election for which will be binding on both parties.

Off-payroll working

A technical change will address an unintended widening of the definition of an intermediary company in the off- payroll working rules legislation.

Changes to the rules regarding the provision of information by parties in the labour supply chain will make it easier for parties in a contractual chain to share information relating to the off-payroll working rules. The changes will allow an intermediary, as well as a worker, to confirm if the rules need to be considered by the client organisation.

The government will also amend a provision relating to fraudulent information to allow HMRC to take action against any UK-based party in the labour supply chain providing fraudulent information.

Tax treatment of business rates repayments

The repayments of business rates relief by some businesses will be deductible for corporation tax and income tax, as previously announced.

Interest and royalties

The legislation that gives effect to the EU Interest and Royalties Directive will be repealed. This legislation currently provides

an exemption from withholding tax on intra-group interest and royalty payments between UK and EU companies. From 1 June 2021 withholding taxes will apply to payments of annual interest and royalties made to EU companies, subject to the terms of the relevant double taxation agreement.

Enterprise management incentives (EMI)

As previously announced, the government will extend until 5 April 2022 the time-limited exception ensuring that employees continue to meet the working time requirements for EMI schemes if they are furloughed or working reduced hours because of COVID-19.

VALUE ADDED TAX

Registration and deregistration thresholds

Until 31 March 2024 the VAT registration threshold will remain at £85,000 and the deregistration threshold will stay at £83,000.

VAT deferral new payment scheme

As previously announced, businesses that deferred VAT payments due between 20 March and 30 June 2020 will be able to pay them in 8 to 11 interest-free equal monthly instalments up to 31 March 2022.

Businesses may opt into the scheme until June 2021 and the number of instalments depends on the date of opting in.

Businesses that do not choose this option must pay deferred VAT by 31 March 2021. A penalty will be charged where the deferred VAT is not paid or there is no arrangement to pay.

Tourism and hospitality

The temporary reduced rate of 5% for hospitality, holiday accommodation and attractions is extended until 30 September

2021. A new reduced rate of 12.5% will apply from 1 October 2021 to 31 March 2022, at which point the rate will revert to the 20% standard rate.

Making tax digital (MTD)

MTD will be extended to all VAT registered businesses with effect from 1 April 2022, as previously announced.

CORONAVIRUS MEASURES

Coronavirus job retention scheme (CJRS)

The CJRS (furlough scheme) will be extended to run until 30 September 2021, providing employees with 80% of their current salary for hours not worked.

Up to the end of June, the current 80% government payment level will be maintained (capped at £2,500 a month), with employers responsible for NICs and pension payments. The government payment will then drop to 70% in July and 60% in August and September (with the monthly cap reducing proportionately).

Self-employed income support scheme (SEISS)

The SEISS will also be extended to September 2021. A fourth SEISS grant will run from 1 February to 30 April, worth 80% of three months’ average profits (capped at £7,500). This grant will be claimable from late April.

A fifth grant, claimable from late July, will cover the period May to September. It will be worth 80% of three months’ average profits where the claimant’s turnover has dropped by 30% or more. Where the fall in turnover is less, the grant will be limited to 30% of profits (capped at £2,850). Eligibility for both grants will be extended to include those who were self-employed in 2019/20 and who have filed a tax return for that year.

Recovery loan scheme

From 6 April 2021, a new recovery loan scheme will provide lenders with a guarantee of 80% on eligible loans between £25,000 and £10 million. The scheme will be open to all businesses, including those that have already received support under the existing COVID-19 guaranteed loan schemes.

Restart grants

The government will provide restart grants in England of up to £6,000 per premises for non-essential retail businesses and up to £18,000 per premises for hospitality, accommodation, leisure, personal care and gyms. Local authorities in England will be given an additional £425 million of discretionary business grant funding.

Business rates reliefs

The 100% business rates relief for eligible retail, hospitality and leisure properties in England will continue to 30 June 2021. It will be followed by 66% business rates relief from 1 July 2021 to 31 March 2022, capped at £2 million per business for properties that were required to be closed on 5 January 2021, or £105,000 per business for other eligible properties. Nurseries will also qualify for relief in the same way as other eligible properties.