This will mean that shortly, any non-resident buying residential property in the UK, who currently owns another home anywhere in the world, will pay an additional 4% SDLT (on top of the standard SDLT rates of 2-12% mentioned below) on the purchase of the property.

You must pay Stamp Duty Land Tax (SDLT) if you buy a property or land over a certain price in the UK. The total value you pay SDLT on (the ‘consideration’) is usually the price you pay for the property/land.

Sometimes it might include another type of payment like:

- goods

- works or services

- release from a debt

- transfer of a debt, including the value of any outstanding mortgage

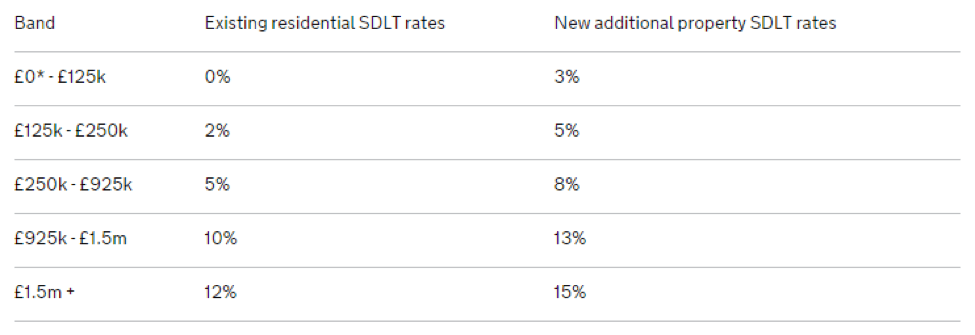

You usually pay SDLT on increasing portions of the property price above £125,000 when you buy residential property, e.g. a house or flat, or above £150,000 when you buy commercial property. The rates range from 2% to 12% for residential properties and 2% to 5% for commercial properties.

The below table shows the current SDLT rates for UK residential property, and the additional 3% charge for buying a second home (note that this is applicable even for property values of less than £125k):

The current additional 3% and future additional 1% SDLT surcharges detailed above are applicable for both individuals and corporate entities.

The current additional 3% and future additional 1% SDLT surcharges detailed above are applicable for both individuals and corporate entities.

Gary Bloch FCCA

Managing Partner

For more information please contact Gary:

gary.bloch@fkgb.co.uk

050 578 9154