Deadlines

HMRC must receive your tax return and any money you owe by the following deadlines –

- Paper tax returns – Midnight 31 October

- Online tax returns – Midnight 31 January

- Pay the tax you owe – Midnight 31 January

If you want HMRC to automatically collect tax you owe from your wages and pension, you must be eligible and submit your online return by 30 December.

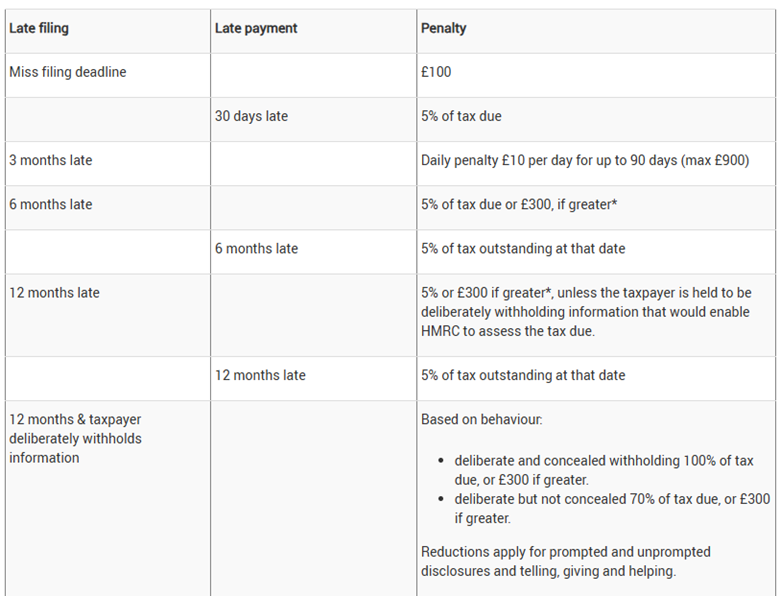

Penalties

There are 2 types of penalties, late filling penalty if you file the tax return after the deadline and late payment penalty if you pay the tax due after the payment deadline.

Late payment example:

Jane was due to make a balancing payment of £10,000 in Income Tax under Self-Assessment for the 2021-22 tax year; it fell due for payment on 31 January 2023. She ignores the reminders and eventually pays her tax in February 2024.

If the tax was not paid penalties accrue as follows:

| Trigger date | Penalty |

| Unpaid by midnight 2 March 2023 | £500 (5%) |

| Unpaid by midnight 2 August 2023 | £500 (5%) |

| Unpaid by midnight 2 February 2024 | £500 (5%) |

Late payment interest

The current late payment and repayment interest rates applied to the main taxes and duties that HMRC currently charges and pays interest on are:

- late payment interest rate — 7.50% from 20 August 2024

- repayment interest rate — 4.00% from 20 August 2024

However, the Chancellor, Rachel Reeves, announced in the Autumn budget of 2024, that late payment interest rate charged on unpaid tax liabilities will increase by 1.5 percentage points from April 6, 2025, so total interest will be 9%.

Changes to your return

You can correct a tax return within 12 months of the Self-Assessment deadline, online or by sending another paper return.

Example

For the 2022 to 2023 tax year, you’ll usually need to change your return by 31 January 2025.

Appeal against a penalty

If HMRC sends you a penalty letter by post, use the appeal form that comes with it or follow the instructions on the letter.

You can get your penalty cancelled if you did not send a tax return because you no longer needed to. Tell HMRC online you do not need to be self-assessed or call the helpline.

Otherwise, to appeal you’ll need:

- the date the penalty was issued

- the date you filed your Self-Assessment tax return

- details of your reasonable excuse for late filing

Reasonable excuses

You can appeal against some penalties if you have a reasonable excuse, for example for your return or payment being late.

A reasonable excuse is something that stopped you meeting a tax obligation that you took reasonable care to meet, for example:

- your partner or another close relative died shortly before the tax return or payment deadline

- you had an unexpected stay in hospital that prevented you from dealing with your tax affairs

- you had a serious or life-threatening illness

- your computer or software failed just before or while you were preparing your online return

- service issues with HM Revenue and Customs (HMRC) online services

- a fire, flood or theft prevented you from completing your tax return

- postal delays that you could not have predicted

- delays related to a disability you have

You must send your return or payment as soon as possible after your reasonable excuse is resolved.

HMRC may consider COVID-19 as a reasonable excuse for missing some tax obligations (such as payments or filing dates).

Explain how you were affected by COVID-19 in your appeal. You must still file the return or make payment as soon as you can.

The following will not be accepted as a reasonable excuse:

- you relied on someone else to send your return and they did not

- your cheque bounced or payment failed because you did not have enough money

- you found the HMRC online system too difficult to use

- you did not get a reminder from HMRC

- you made a mistake on your tax return

Please also read FKGB blog on payment on account: Payments on Accounts – Self Assessment | FKGB Accounting