An Introduction to Investors’ Relief

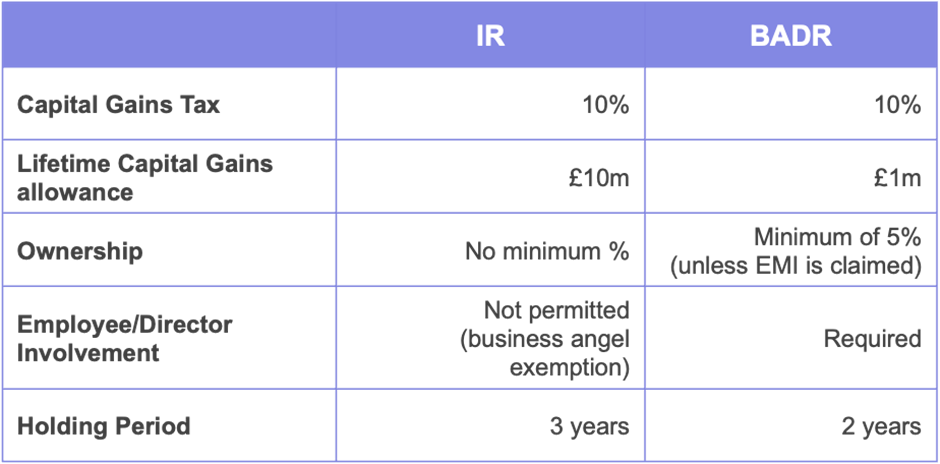

Investors’ relief is a relatively new scheme (introduced in 2016) that draws many parallels from Business Asset Disposal Relief (BADR- formerly Entrepreneur’s Relief). To claim BADR you need to own more than 5% of voting and ordinary shares, which becomes problematic as this automatically disqualifies all but a few individuals. In order to combat this unfairness, Investors’ relief was created which does not have an ownership cap as a condition.

What is Investors’ Relief?

Investors’ relief offers a reduction in capital gains tax to those disposing of qualifying shares. It offers many of the same benefits as BADR, but with a significantly higher lifetime allowance and a few caveats such as not being allowed to be an employee/have direct involvement, and a slightly longer holding period.

Am I eligible?

HMRC’s official guidance can be found here, however, the brief qualifying criteria can be found below and the relief is only available to individuals and some trustees of settlement.

- You have owned the shares for at least three years

- The shares constitute ordinary shares

- None of the company’s shares are listed on a stock exchange

- You subscribed for them in cash, and they were fully paid up when issued

- The company is a trading company or the holding company of a trading group

- Neither you nor any person connected with you is an employee of the company or of a company connected with it

How much is the relief and what is the maximum you can claim?

The relief decreases all qualifying IR share sales to just 10% in capital gains tax which could lead to a potential lifetime saving of £1m in overall tax.

Unlike BADR where the lifetime allowance is only £1m, the lifetime allowance that you can claim for IR is £10m.

What if I work for the company?

The good news is that there is still a possibility to reduce capital gains tax to 10% on share sales, however, this would require a certain amount of tax planning to have been conducted. Either you own 5% of share capital and voting rights or you are engaged in an HMRC approved EMI scheme. If either of these is the case you may be eligible for Business Asset Disposal Relief (formerly Entrepreneur’s relief).

Difference between Business Asset Disposal Relief and Investors’ Relief

Final Thoughts

- Investor’s relief is a useful tool if you know how to utilise it.

- It offers 10 times the relief of the more widely known BADR (formerly entrepreneurs’ relief).

- Unlike BADR, there is no ownership limit to claim relief.

- The scheme could potentially save you over £1m in tax over your lifetime.