The National Insurance Contributions (Reductions in Rates) Bill 2023-24 was introduced on 23 November 2023. The Bill implements three changes to National Insurance contributions (NICs) which were announced by Chancellor Jeremy Hunt in the 2023 Autumn Statement.

These changes are:

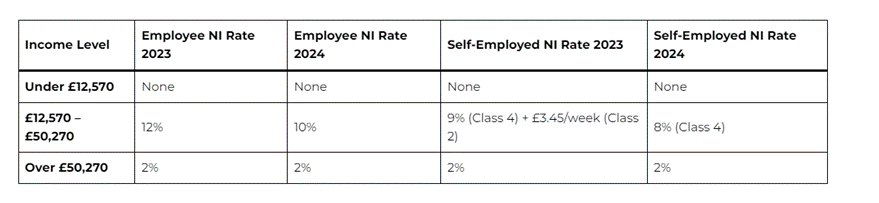

- A cut in the main rate of NICs paid by employees (‘primary Class 1 NICs’) from 12% to 10%. This rate cut would apply from 6 January 2024.

- A cut in the main rate of NICs paid by the self-employed (‘Class 4 NICs’) from 9% to 8%. This rate cut would apply from 6 April 2024.

- Cancelling the requirement of the self-employed to pay the flat rate NICs charge (‘Class 2 NICs’), which applies when someone’s annual profit exceeds a set threshold (the ‘lower profits threshold’). This threshold is currently £12,570. This change would take effect from 6 April 2024.

These measures would extend and apply to the whole of the UK.

How would the Bill affect taxpayers?

The Office for Budget Responsibility (OBR) estimate this tax cut will benefit around 27 million employees and over 2 million self-employed people overall.

The 2% cut in the main rate of NICs for employees is estimated to benefit a basis rate taxpayer by £304 annually, £647 for higher-rate taxpayers and £707 for additional-rate taxpayers.

The 1% cut in the main rate of NICs for the self-employed is estimated to benefit a basis rate taxpayer by £117 annually,£322 for higher-rate taxpayers and £358 for additional-rate taxpayers.

Removing the requirement to pay Class 2 NICs for self-employed individuals with profits above the lower profit’s threshold is estimated to benefit 1.9 million individuals in 2024/25. The average annual gain is estimated to be £186 per person for this group.

NI Breakdown – Comparison