Automatic enrolment is when an employee who meets certain requirements is made a member of a workplace pension scheme without needing to ask to be part of it. In the past, it was up to workers to decide whether they wanted to join their employer’s pension scheme but since 2012, employers have been required to automatically enrol their eligible workers into a workplace pension scheme.

Who will be automatically enrolled?

Whether you work full-time or part-time, your employer will have to enrol you in a workplace pension scheme if you meet these auto enrolment rules:

- You work in the UK (including seafarers residing in the UK)

- You aren’t already in a suitable workplace pension scheme

- You are at least 22 years old, but under State Pension age

Do I have any choice about being enrolled?

You can opt out of your employer’s workplace pension scheme after you’ve been enrolled but if you do, you’ll lose out on your employer’s contribution to your pension, as well as the government’s contribution in the form of tax relief.

If you decide to opt out within a month of being enrolled, any payments you’ve made into your pension pot during this time will be refunded to you. After the first month, you can still opt out at any time, but any payments you’ve made will stay in your pension pot for retirement rather than be refunded.

You can re-join your employer’s workplace pension scheme later if you want to.

By law, your employer must re-enrol you back into the scheme approximately every three years. This is if you still meet the eligibility criteria.

How much will I have to contribute?

There is a minimum total amount that must be contributed by you, your employer, and the government (in the form of tax relief).

These minimums are generally: 5% from you (which includes tax relief) and 3% from your employer.

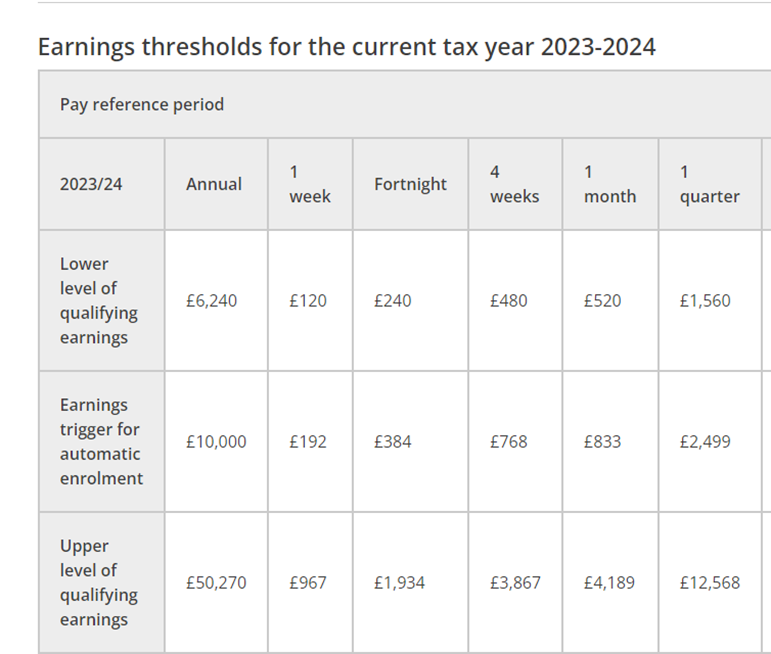

The minimum contribution applies to anything you earn over £6,240 up to a limit of £50,270 (in the tax year 2021/22). This slice of your earnings is known as ‘qualifying earnings’.

Earnings thresholds for 2023/24

The minimum contribution applies to anything you earn over £520 up to a limit of £4,189 per month. This slice of your earnings is known as ‘qualifying earnings’, so maximum employee contribution per month will be £146.76.