If your company provides you with a company car, you may be wondering what the extra tax that you will have to pay on this benefit will be.

Step 1 – Defining list price of the car

The P11D list price of a car is the manufacturer’s recommended retail price (RRP) on the day before the car was first registered — not the price your employer paid.

It includes:

- Basic price of the car

- Factory-fitted options (over £100)

- Delivery charges

- VAT

It excludes:

- Registration fees

- Road tax

- Fuel

This list price is used to calculate the taxable benefit in kind for company car drivers.

Capital contributions (payments made by the employee towards the cost of the car and accessories) are deducted from the price of the car and accessories (maximum deduction £5,000)

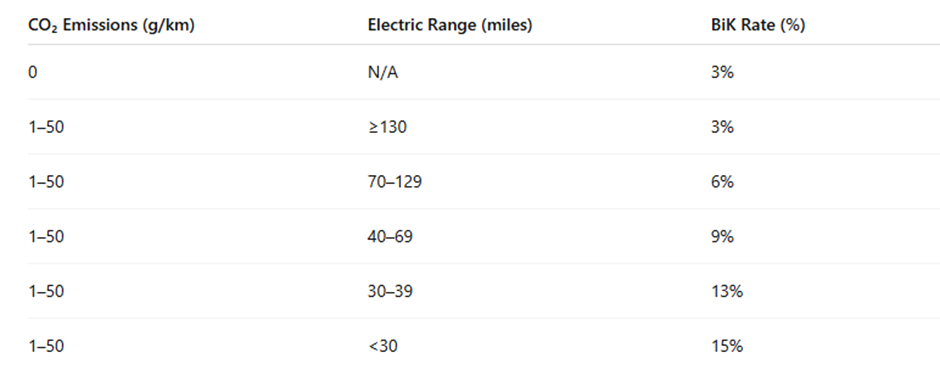

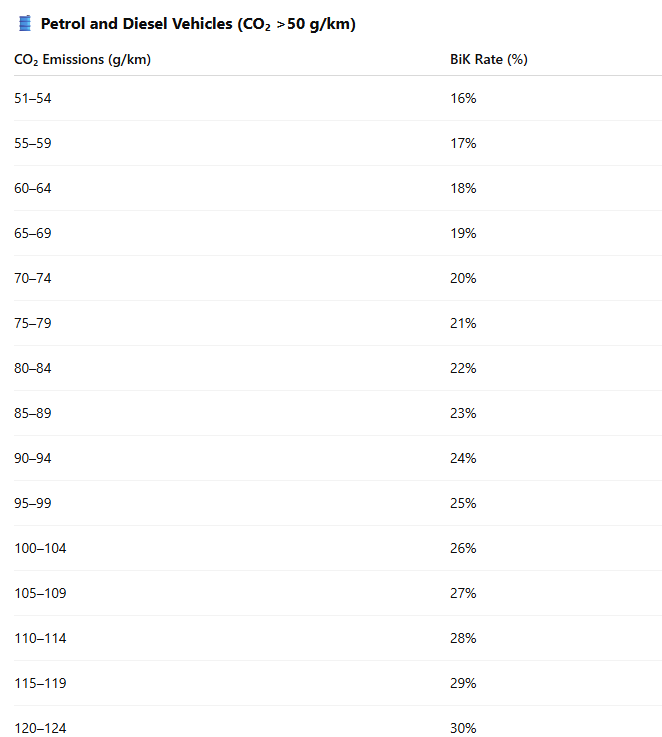

Step 2 – Checking the carbon dioxide (CO2) emissions

The taxable benefit depends on the carbon dioxide (CO2) emissions of the car, as shown in the following charts –

Electric and Low-Emission Vehicles (0–50 g/km CO₂) – 2025-26 Value

BMW 330e M Sport (Plug-In Hybrid), with CO₂ Emissions: ~36 g/km, Electric-Only Range: ~37–39 miles (WLTP), Electric-Only Range: ~37–39 miles (WLTP)

List Price: £47,000

Bik Rate (2025–26): 13% (for electric range 30–39 miles)

Taxable Benefit: £6,100. If you are 40% taxpayer, you will need to pay £2,444 extra tax on this benefit.

Petrol and Diesel Vehicles (CO₂ >50 g/km)

The above rates will change in 2026-27 tax year, please check the HMRC website for future years – https://www.gov.uk/government/publications/check-future-rates-for-petrol-powered-and-hybrid-powered-company-cars/co2-emissions-tables-of-rates?utm_source=chatgpt.com.