There are various tax allowances that maybe relevant when calculating your self-employment business expenses for your UK tax return. These allowances are only relevant if you use the accruals basis when presenting your income/expenses, not the cash basis option.

- Annual investment allowance

- First year allowance

- Writing down allowance

Annual investment allowance (AIA)

If you purchase items for your business that will last for 2 years or more, for example office furniture, computer or company van, these are considered capital purchases, and you can choice to claim the entire expense in the tax year this expense occurred using AIA. The limit is up to £1 million of capital expenses per tax year.

Example

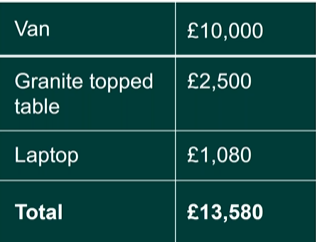

Sophie has a flower shop, and she purchases the following capital items –

- a van for £10,000 (can either be brand new or 2nd hand) – 100% business usage.

- granite topped table for £2,500 – 100% business usage.

- and a laptop for £1,200 – 90% business usage, can claim £1,080 (90% of the expense).

all these items are expected to last at least 2 years.

Sophie can claim the following in the annual investment allowance section on her tax return –

If Sophie sells the van after 2 years, for £7,200, this amount needs to be declared as income on the next tax return, as she claimed the entire amount as expense in previous tax years. This needs to be declared in total balances charges section of the tax return.

There are certain circumstances where you cannot claim AIA –

- if you owned this item for another reason before you started using it in your business.

- Items given to you for your business.

- Business cars (unlike vans)

- If you have exceeded £1 million in the tax year.

In these circumstances, you may be able to claim either the writing down allowance or first year allowance.

First year allowance (FYA)

You can claim the entirety of the expenditure in the first year that the item was purchased, it is not limited to the first year of your business.

Writing down allowance (WDA)

As explained above, if you used an item for other purposes before using it solely for business purposes, you cannot claim AIA, rather will need to claim WDA.

Example

Sam purchased a van for personal usage and after a few years decided to use the van solely for his business. The van’s value at the time he decides to use it for business usage is £1,400. The WDA rate is 18% on these types of items in the “main pool”, so Sam can claim the following –

- Year 1 – 18% of £1,400 = £252. Ending balance going into year 2 is £1,148.

- Year 2 – 18% of £1,148 = £207. Ending balance going into year 3 is £941.

- Year 3 – as the remaining balance is less than £1,000, Sam can claim “small pools allowance” and can claim the entire £941 in year 3.