Introduction

If a director or employee has a loan from the company and:

- The loan exceeds £10,000 at any point in the tax year, and

- No interest is paid, or interest is paid below HMRC’s official rate,

then the difference is treated as a taxable benefit and must be reported on the P11D form.

How is the benefit calculated?

There are two accepted methods for calculating the benefit-in-kind:

- Average Method (common method unless repayment patterns are irregular):

- 2024/25 HMRC official rate: 2.25%

- Applies if loan is steady throughout the year (no major fluctuations).

Example (2024-25 tax year)

A director has:

- £30,000 loan on 6 April 2024

- £40,000 loan on 5 April 2025

- Pays no interest

- Average balance = (£30,000 + £40,000) / 2 = £35,000

BIK = £35,000 × 2.25% = £787.50

This £787.50 is reported as a benefit on the P11D, and:

- The director pays income tax on this amount, and

- The employer pays Class 1A NICs at 13.8% on the same amount.

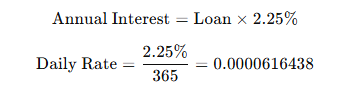

- Strict Method (more precise, if loan changes significantly):

- Calculate the daily balance for each day of the tax year.

- Apply the daily interest using HMRC’s rate to each day.

- Total the interest across the year.

Example (2024-25 tax year)

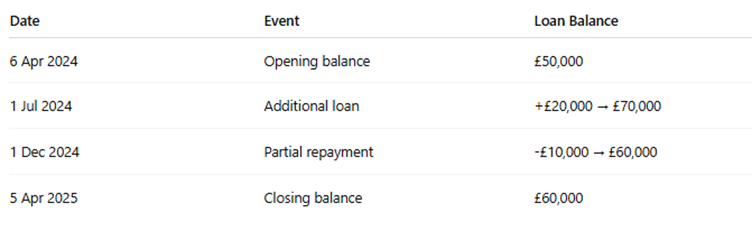

A director has the following loan transactions from their company:

Step 1: Calculate interest per day

Step 2: Calculate each period

Period 1: 6 Apr – 30 Jun (86 days)

Loan: £50,000

Interest: 50,000×0.0000616438×86 = £265.08

Period 2: 1 Jul – 30 Nov (153 days)

Loan: £70,000

70,000×0.0000616438×153=£660

Period 3: 1 Dec – 5 Apr (126 days)

Loan: £60,000

60,000×0.0000616438×126= 466.01

Total BIK: £265.08+£660.59+£466.01=£1,391.68

This £1,391.68 is reported as a benefit on the P11D, and:

- The director pays income tax on this amount, and

- The employer pays Class 1A NICs at 13.8% on the same amount.